‘Crypto paradise’ Singapore stung by high-profile collapses

The international manhunt for Do Kwon, co-founder of collapsed cryptocurrency operator Terraform Labs, has put the spotlight on Singapore, whose reputation has taken a hit following the failure of several digital asset funds with links to the city-state.

Not only was Kwon’s company, whose stablecoin terraUSD imploded in May, registered in Singapore, but Korean prosecutors believe he travelled to the city-state in April.

Kwon last week showed Singapore as his location on Twitter, writing that he was making “zero effort” to hide. Singapore police have said Kwon is not in the city-state.

Kwon’s case is not the only high-profile crypto controversy unfolding in Singapore, which was until recently pitching itself as a digital asset-friendly destination in competition with global rivals Dubai and Zurich.

Crypto executives and experts said the lengthening list of scandals and collapses has tarnished Singapore’s reputation after officials touted its stability, sophisticated regulation and tax-friendliness as an advantage for crypto companies and investors.

“The reputational damage over the last six months is a lot more serious than has been let on,” said Kelvin Low, a law professor at the National University of Singapore. “Every time one of these companies is brought up, they are mentioned [as being] based in Singapore.”

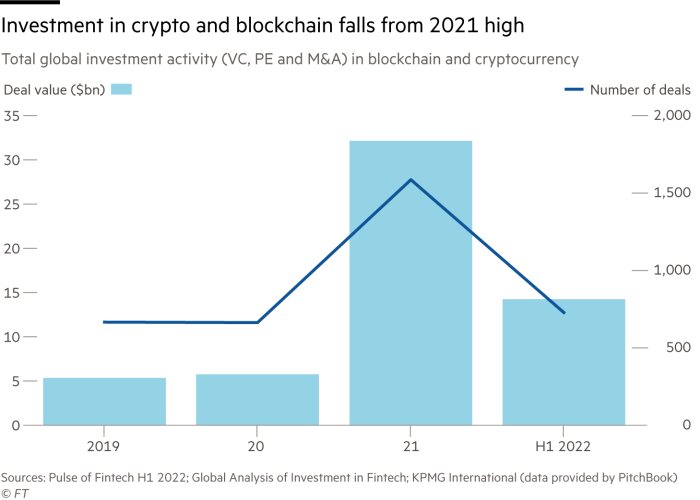

Previously Singapore was some kind of crypto paradise . . . times changed

Some of the biggest crypto collapses can be traced through Singapore, which had attracted digital asset companies from all over the world.

“Singapore has the most liberal regulatory environment after Switzerland in terms of crypto investment,” Kim Hyoung-joong, head of the Cryptocurrency Research Center at Korea University.

“Crypto players prefer to operate in Singapore because of transparent regulations and their easy access to investors for funding,” said Kim.

Three Arrows Capital, a crypto hedge fund that collapsed in June, started as a registered fund management company in Singapore.

Management of the company’s sole fund later shifted to an offshore entity in the British Virgin Islands. Co-founders Su Zhu and Kyle Davies have not revealed their location since Three Arrows’ failure.

Singapore’s regulator reprimanded Three Arrows for providing false information and breaching certain asset management thresholds. It added that it was assessing whether further regulatory breaches occurred.

Hodlnaut, a Singaporean crypto lender that received in-principle licensing approval from the Monetary Authority of Singapore, halted withdrawals and cut the majority of its employees earlier this year.

In August, Hodlnaut was placed under interim judicial management. The company said this decision would “provide a better chance of recovery”. Singapore police said that they were “looking into” Hodlnaut.

Singapore police did not investigate the terraUSD collapse despite a complaint being filed, according to local media. Police did not respond to a request for comment regarding Terraform Labs and Kwon.

MAS said “none of these troubled companies are licensed by the Monetary Authority of Singapore” under its Payment Services Act, which regulates payments systems, and so were not under its jurisdiction.

It said Three Arrows Capital had “ceased to manage funds [in Singapore] prior to the problems leading to its insolvency”. It added that Hodlnaut had withdrawn its licence application, so the “suspension of services is not in breach” of Singapore regulations.

“In Singapore, as is the case in all other jurisdictions, not all activities related to cryptocurrencies are regulated,” said MAS, adding that its “evolving regulatory approach makes Singapore one of the most comprehensive in managing the risks of digital assets”.

As the crypto crunch set in, regulators in Singapore have started taking a tougher line, with officials promising to be “unrelentingly hard” on bad behaviour in the sector.

But experts said Singapore was not doing enough to punish or investigate possible fraud as a crisis has swept through the digital asset industry, causing an avalanche of losses for retail investors.

“I do think there is an extent to which [Singapore] is willing to say one thing and do something quite different,” an executive at a crypto company active in Singapore said.

The same executive said they believe Singapore was in a “tight spot” in trying to balance being seen as a “serious player in the world economy” and “trying to promote themselves as a hub for innovation in a nascent industry which is clearly showing itself to have more and more bad actors”.

In August, MAS managing director Ravi Menon distanced the regulator from the scandals and said it would take “further measures to reduce consumer harm”.

Most steps have been preventive measures to protect Singaporean retail investors, such as a crackdown on advertising, rather than disciplinary ones.

The changing tone from officials including Menon has caused some crypto companies to reassess their Singapore operations.

Binance, the world’s largest crypto exchange, has abandoned plans to make the city a hub despite its chief executive Changpeng Zhao living there for much of 2021. Last year, it was also placed on the MAS investor alert list.

“Singapore is not a big focus for us,” said Gleb Kostarev, regional head of Asia for Binance. “A lot depends on regulation . . . previously Singapore was some kind of like crypto paradise . . . times changed.”

Others have come to the defence of Singapore’s status as a crypto hub, suggesting it would be unfair to blame the city-state.

“I think it’s somewhat also unfair to try to put all the onus and responsibility on the regulators, when often the party to blame in many instances are the crypto markets players who frankly, in many cases, should know better,” said one individual familiar with the matter.

Teresa Goody Guillén, partner at US law firm BakerHostetler, said an Interpol red notice for Kwon was “unlikely to have an impact on legitimate companies’ interest in forming or operating in Singapore”.

The crypto industry “does not appear to react negatively to law enforcement investigating allegations of criminal activity, fraud, and the like,” she added.

ChainUp, a blockchain company that offers technology to crypto exchanges and other clients said it was expanding in the city-state.

The start-up relocated its headquarters from China to Singapore in 2019 as Beijing was signalling it was clamping down on the sector.

“I am confident in the approach of regulators,” said Sailor Zhong, ChainUp’s chief executive.

“No one country can do it all and it is hard for Singapore’s government to enforce rule of law for companies with operations abroad.”